The field looked like a painting the summer the bees arrived. White clover foamed at the edges of the old wire fence, and the retired school custodian—let’s call him Walter—stood with his hands in his pockets, breathing in the faint sweetness of blossoms and smoker’s ash. The beekeeper, a younger man with sunburnt forearms and a rusted pickup, had just finished setting the hives in a neat row, each box humming like a tiny engine. They shook hands in the shade of the lone maple tree, the air thick with late-afternoon heat and the lazy drift of bees discovering their new world.

No contract. No rent. No talk of money at all. Just a favor. Walter had a bit of unused land behind his modest house, and the beekeeper needed a quiet place away from roads and pesticides. It felt like the kind of neighborly act that should earn you good karma, not a bill.

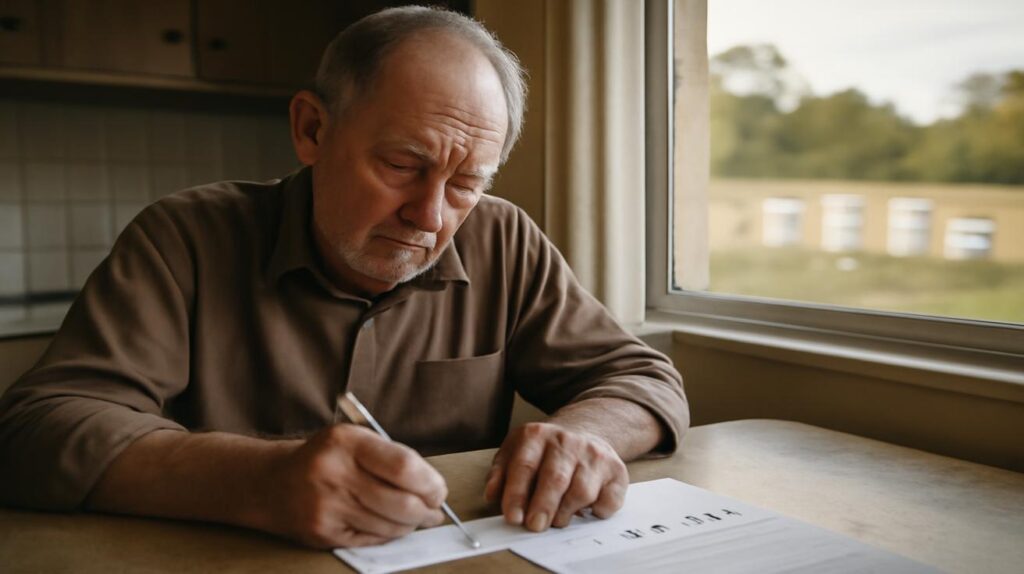

Yet, a year later, it was not a jar of honey or a thank-you card that showed up in Walter’s mailbox. It was a letter from the tax office.

The Letter That Soured the Honey

It arrived in a windowed envelope, printed on thick, official paper that feels heavier than it should—like bad news disguised as stationery. Walter sat at his kitchen table, coffee cooling beside him, and read the words that made his jaw tighten:

“Assessment of agricultural land tax for the year…”

Tax. On what, exactly? He hadn’t sold a single jar of honey. There were no invoices, no farm stand by the road, no extra line in his bank statement. Just a piece of ground he’d lent, free of charge, to a man with bees and hope and not much else.

As Walter read on, it became clear: the government didn’t care that he’d earned nothing. The land was being used for agriculture—beekeeping, in this case—and under the rules, that meant agricultural tax.

The bees were his guest’s. The hives were his guest’s. The income, if there was any, was his guest’s. But the land was his, and in the eyes of the law, that made him responsible.

There is a special kind of sting in paying tax on a kindness.

The Quiet Logic of the Taxman

At first glance, it feels outrageously unfair. How can someone be taxed for “earning” nothing? That question echoed around Walter’s kitchen, picking up speed with each step he paced. But tax systems are like root systems in an old forest—hidden, intricate, and rarely built around individual feelings of fairness. They are built to be broad, blunt, and—above all—simple to administer.

From the tax authority’s perspective, the story is different and very straightforward:

- The land is being used for an agricultural purpose (beekeeping).

- The owner of the land is responsible for land-related taxes.

- Whether the owner personally profits is not the main concern.

Some laws even treat the potential for income as enough reason to levy tax, especially when land is being used in a way that fits agricultural or commercial categories. The assumption is that land used productively is part of the economic fabric—whether or not the threads of profit reach the landowner directly.

To tax officials, it’s about the land’s status, not the landowner’s story.

And that is exactly where things begin to feel uneasy. Because while the tax code needs simple rules, life has a way of slipping between them, trailing stories of generosity, hardship, and good intentions.

The Retiree’s Perspective: A Different Kind of Balance Sheet

Walter didn’t keep a ledger, but if he had, the math would be simple:

- Income from the land: 0

- Cost of owning the land: ongoing

- New tax assessment: an unpleasant surprise

He lived on a fixed income. Pensions don’t grow when bees move in next door. When you’ve spent your life saving carefully—patching up cars instead of buying new ones, saying no to trips, fixing your own leaky gutters—an unexpected tax bill feels less like a civic duty and more like a betrayal.

Because in his mind, this was not a business decision. This was helping a neighbor, helping pollinators, helping the land stay alive instead of turning into a mowed, silent lawn. It was doing something right.

But the tax system, blunt and clinical, has no box for “right.” It has boxes for “use,” for “category,” for “owner.”

Fairness, Seen From Two Directions

Fairness is a slippery word. It bends depending on where you stand.

From Walter’s side of the fence, fairness means: “I did something kind, I earned nothing, I shoulder the cost alone. That can’t be right.”

From the taxman’s side, fairness is more structural: “If we allow landowners to dodge agricultural tax by saying they ‘lent’ land for free, we open a door for abuse. Some will exploit it. We need a rule that applies the same to everyone, simple and enforceable.”

So you have two truths facing each other across a field of clover:

- Personal fairness: recognizing intention, context, and outcome.

- Systemic fairness: applying the same rule to every similar situation.

Modern tax systems almost always err toward the second. They have to, or they collapse under the weight of individual exceptions. But in doing so, they inevitably step on the toes of people like Walter, whose acts of goodwill are treated no differently than quiet, informal business arrangements.

Put more bluntly: the law cannot tell the difference between a generous favor and a cleverly disguised rent-free deal.

The Beekeeper in the Middle

It’s easy to cast the beekeeper as the lucky beneficiary here: free land, no tax, just jars of golden income. But his story is not always shiny either.

Many small-scale beekeepers operate on razor-thin margins. Winter losses, rising costs, and chemical exposure can wipe out entire colonies. They often depend on kindness from landowners to survive at all—odd corners of fields, vacant lots, or back paddocks where their bees can forage without complaint.

In an ideal world, that kindness wouldn’t carry a hidden financial penalty for the person offering it. But in reality, both men are squeezed by rules that were not written with their small-scale collaboration in mind.

The beekeeper carries the risk of disease, weather, and failing honey prices. The landowner carries the weight of legal responsibility and tax classification. Between them lies a handshake that the system struggles to recognize.

The Silent Contract: Responsibility Without Reward

One of the more unsettling truths about owning land is that responsibility often sticks to you whether you like it or not. Even when you hand over the use of your land, the law rarely lets you hand over the responsibility as easily.

Think of it this way: the moment the hives were placed on Walter’s property, he entered into an invisible, unspoken contract with the state. It went something like this:

You may allow agricultural use of your land. In return, you accept that your land will be treated as agricultural for tax purposes, and we will expect you to pay accordingly.

There’s no signature, no ink. Just the quiet reclassification of the land in a database far away from the hum of bees and the creak of old fences. By letting those boxes of bees sit there, Walter unintentionally stepped into a regulatory category—far more binding than a neighborly handshake.

That is the quiet battle: goodwill versus systems that recognize only categories, not kindness.

When Goodwill Meets the Tax Code

If you strip away the human story and look only at structures, what happened to Walter follows a predictable pattern:

- Land is lent, not leased: no formal income, no contract, just an agreement.

- Land is put to an agricultural use (beekeeping counts in many jurisdictions).

- Tax authorities classify it based on use, not profit.

- Landowner remains the party on the official record and is therefore billed.

From a legal standpoint, it’s clean, almost elegant. From a human one, it’s messy and frustrating.

To understand how this tension plays out, it helps to look at all three perspectives side by side:

| Perspective | How the Situation Looks | Sense of Fairness |

|---|---|---|

| Retiree Landowner | Lent unused land out of kindness; no income, only extra cost. | Feels punished for being generous. |

| Beekeeper | Relies on free land to keep a fragile business alive. | Grateful, but uneasy knowing the favor carries a hidden price. |

| Tax Authority | Sees agricultural use of land by its legal owner. | Believes equal rules for all use-cases is the fairest system-wide. |

All three are acting rationally. All three can defend their position. Yet only one of them has the power to send legally enforceable letters.

Could It Be Done Differently?

It’s tempting to say the solution is simple: just exempt small, non-commercial uses, or exempt retirees who earn nothing from the activity. But every exemption is another root tunneling under the forest of rules, another potential loophole for the clever and the unscrupulous.

Designing fairness into tax law is like trying to plant wildflowers in straight rows. The nature of life keeps rearranging the pattern.

Still, there are gentler paths that could soften the sting in stories like Walter’s:

- Clearer public guidance: Simple, accessible explanations that warn landowners: “If you allow agricultural use—even for free—here’s what that means for your taxes.” Many people stumble into tax consequences without any warning.

- Optional cost-sharing: Landowners and beekeepers could agree—on paper—that the beekeeper will reimburse any additional tax costs. It doesn’t change the legal duty, but it balances the practical burden.

- Scaled thresholds: Some systems already have minimum thresholds based on scale or income. Where they don’t, introducing them can help separate genuine micro-collaborations from disguised commercial operations.

- Non-monetary incentives: Instead of direct tax breaks, governments might provide small grants, advisory support, or recognition programs for landowners who host pollinators or biodiversity-supporting activities.

These measures won’t fix every case, but they can nudge the system closer to something that feels fair from more angles at once.

The Emotional Cost of a Tax Bill

There is another layer that never makes it into official calculations: what happens to neighborliness when a tax bill arrives where gratitude was expected?

For some, it’s enough to make them vow: “Never again.” No more hives on the back lot. No more community garden in the front field. No more letting the youth group use the meadow for camping. If every act of generosity risks dragging you into a tangle of classifications and costs, the safest choice becomes silence and an empty field.

This is the hidden danger beneath the surface of Walter’s story: not just his frustration, but the quiet retreat of goodwill from public life.

Because when systems don’t recognize or protect good intentions—even modestly—they send an unspoken message: be careful whom you help, and how.

The Bees Don’t Care Who Pays

Walk back out to the field in late summer. The goldenrod flares in dense yellow spikes, and the air trembles with wings. The bees don’t know about the tax bill. They don’t know whose name is on the land registry or who had to raid their grocery budget to pay an assessment they never expected.

They move from flower to flower, repeating the same ancient logic: gather, return, repeat. Pollinate as you go. Life doesn’t pause to check which human categories have been applied to the land it depends on.

In their own indifferent way, the bees reveal a truth: the benefits of certain acts ripple outwards, while their costs can settle heavily on a single pair of shoulders.

Walter’s land, once just a mown patch behind a quiet house, became part of a much wider ecological story. The bees helped nearby orchards, wildflowers, gardens. The beekeeper’s hives supported a local food system that others enjoyed. Yet, when the time came to tally up the numbers, the only new cost line that appeared belonged to Walter.

Maybe justice, in a deeper sense, would notice that asymmetry.

Responsibility Without Bitterness

So why must the retiree pay agricultural tax, despite earning nothing? Because the system anchors responsibility in ownership, not in profit or intention. The land is his. The use is agricultural. The consequence, by design, falls on him.

But understanding that doesn’t mean shrugging and accepting bitterness as the only possible response. It can also mean:

- Asking more questions before offering land for use—what might this mean legally and financially?

- Openly discussing tax with the person you’re helping—will they share the burden if it arises?

- Advocating, where possible, for policies that invite collaboration instead of punishing it.

Responsibility can be carried with eyes open. Bitterness tends to grow when it is forced into your hands in an unmarked envelope.

What This Says About Us

In the end, the story of a retiree, a beekeeper, and a tax bill is not really about paperwork. It is about the uneasy fit between our instinct for mutual help and the machinery we’ve built to govern large, anonymous societies.

We like to imagine that if we act in good faith—if our hearts are decent and our motives unselfish—the world will respond in kind. And often, at the scale of a single street or field, that’s true. The beekeeper brings honey. The neighbor helps mend the fence. The school custodian-turned-landowner lets bees stay on his land, just to see wildflowers dance a little higher in the breeze.

But above that, in the airy heights where forms are designed and rules approved, human stories blur into categories. Land is land. Use is use. Owners are taxpayers. And the small, bright details—arthritic hands offering land for nothing, the soft pride of helping bees survive—fade out of view.

What this tension asks of us is simple, if not easy: to remember that behind every tidy rule is a messy field, and behind every tax bill is a kitchen table where someone will sit, reading, and wonder whether kindness was a mistake.

It asks lawmakers to imagine the faces behind the forms. It asks citizens to learn the edges of their responsibilities, so that generosity can be offered wisely, not blindly. And it invites all of us to keep having these quiet, stubborn conversations about fairness—around kitchen tables, in parliament halls, and yes, out by the humming hives where the real work of life is always underway.

The bees will keep moving from flower to flower regardless. The question is whether, in the years ahead, there will still be people willing to open their gates and say: “Yes, you can use my land”—even knowing that somewhere far away, a system that cannot hear the hum of wings may still send a bill.

Frequently Asked Questions

Why does the landowner have to pay agricultural tax if they earn nothing?

Because most tax systems attach land-related taxes to ownership and use, not to profit. If your land is used for agriculture—such as hosting beehives—it may fall into an agricultural tax category, even if you receive no rent or income.

Can a private agreement with the beekeeper change who the tax authority charges?

No. A private agreement can share or shift the cost between you, but the legal responsibility toward the tax authority normally remains with the landowner, whose name is on the official records.

Is beekeeping always considered agriculture for tax purposes?

In many jurisdictions, yes. Beekeeping is typically treated as an agricultural or farming activity because it involves the production of a food product and the management of livestock (bees). Details, however, depend on local laws.

How can a landowner avoid unexpected tax surprises in situations like this?

Before lending land, speak with a local tax adviser or your tax office, ask how different uses change your land’s classification, and consider putting a written agreement in place with the user that addresses potential tax costs.

Does this mean people shouldn’t lend land for beekeeping or similar activities?

Not necessarily. It means they should do so with clear eyes and good information. Understanding the possible tax implications—and discussing cost-sharing with the user—can turn a painful surprise into a manageable, intentional choice.